[This blog was written by Chad Becker, the Founder of Arco Real Estate Solutions]

GSA Lease Term – What a difference a few years can make!

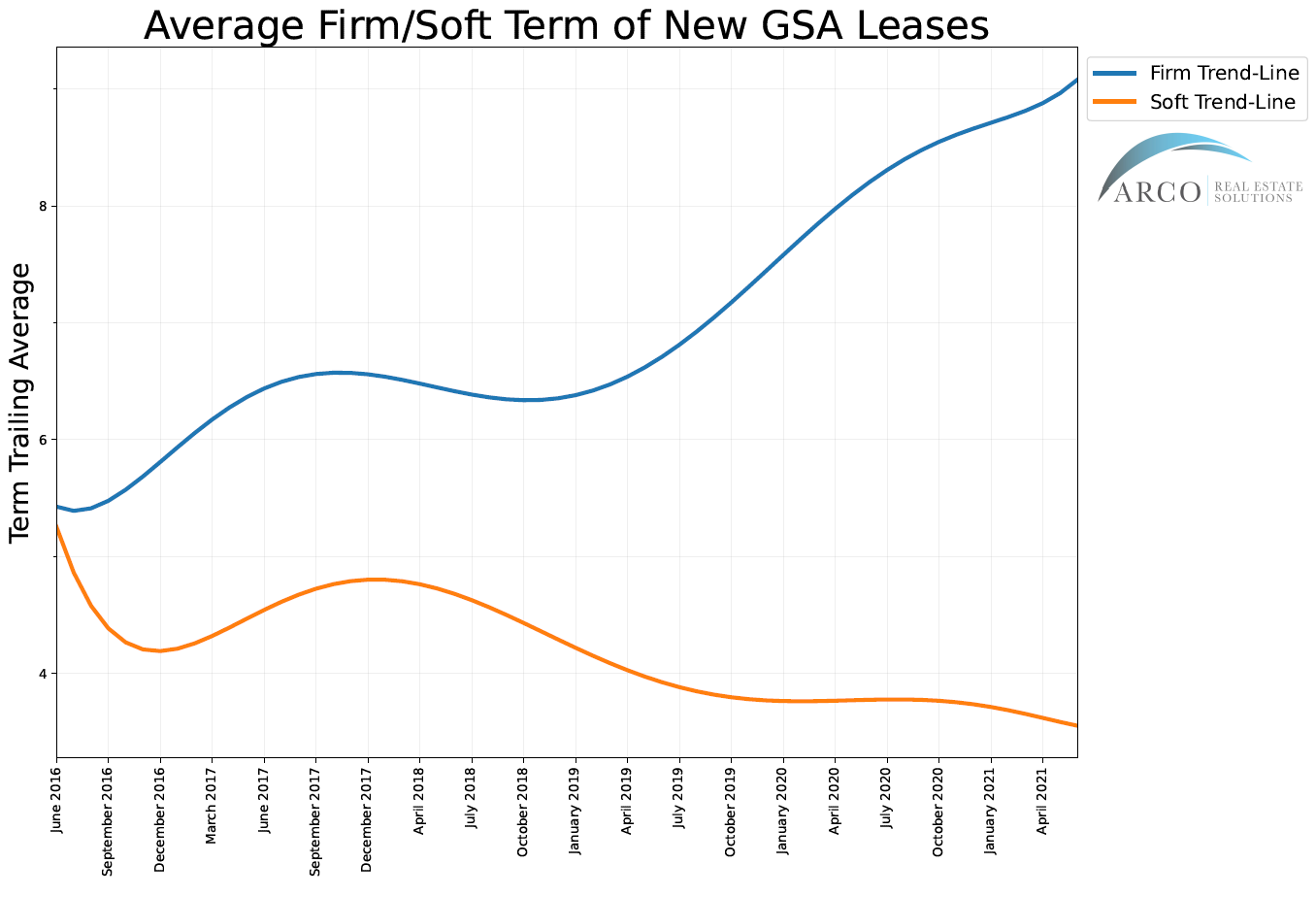

For those of us who follow the Federal Government leasing sector closely, the following graph should not come as a surprise based on what we have been experiencing in the market over the last several years.

However, observing something anecdotally did not prepare me for what we were able to objectively demonstrate after analyzing over 440,000 rows of data provided by the General Services Administration. The graph below is the result of this effort.

The following graph shows GSA has steadily been increasing its firm term in new leases while at the same time decreasing its reliance of soft term that provided very little value.

Before we dive into a bit of analysis, perhaps a quick history of why and how this happened is in order.

On April 20, 2016, the then Assistant Commissioner for the Office of Leasing for the Public Buildings Service, Chris Wisner, signed and put into affect a Leasing Alert with three stated purposes:

- Obtain lower rental rates by better leveraging GSA’s financial strength and its 20 year lease acquisition authority by entering into longer leases where appropriate;

- Reduce the number of lease procurements and the resulting workload burden on regions through the use of longer lease term strategies; and

- Implement these strategies in a manner that does not result in a material increase in vacant leased space.

While it is true that there is a long history of industry input and other factors that led to the release of this leasing alert, the fact remains that this stated policy direction was a significant departure from decades of an almost assembly line approach of producing leases with terms of 10 years / 5 years firm. The 10 /5 approach became dogma within the GSA leasing community despite that fact that I never heard a compelling origin story. “That’s just how we do it”, was the common refrain while I worked in GSA leasing. And to be clear, I too pumped out my fair share of 10/5 leases while at GSA without considering for even a moment if the term made any strategic sense.

In addition to the industry input, GSA’s own analysis pointed out an interesting fact. While GSA was busy producing 10 year leases with 5 years of firm term, they were actually occupying the same location for over 20 years on average.

Based on this observation alone, it begged two questions:

- Why would GSA not take advantage of longer terms in order to negotiate more competitive rents compared to their private sector peers?

- Does the Government actually need 5 years of “soft-term”?

The questions were later addressed by GSA with two major pushes. Increase term and reduce the amount of term that was cancellable, or soft.

While there is a lot to dissect here, we will forego the deep dive for now and return to our original graph.

Based on GSA’s own data, as provided in their monthly leased inventory spreadsheets, it is clear that they, as an agency, are achieving exactly what they have set out to do.

The trends presented above demonstrate that since the release of the above-referenced leasing alert, and to some extent the nationwide release of AAAP which only allows for two years of soft-term, GSA has been on a clear and steady path of increasing overall term while decreasing its reliance on unnecessary and burdensome extended soft-term periods.

While this is outstanding news for GSA and for the industry at large, it has certainly come with some unforeseen consequences that are becoming more and more apparent.

I will cover these consequences in later articles, but for now, I will close by congratulating GSA on listening to feedback from stakeholders, reviewing its own data, setting a vision for course correction, and executing in a meaningful way.

See this original article posted on Linked in: https://www.linkedin.com/pulse/gsa-lease-term-what-difference-few-years-can-make-chad-becker/